Unraveling the World of Jumbo Loan Mortgage Rates 2024

Introduction

Have you ever dreamed of owning a luxurious home with all the bells and whistles? Or perhaps you’re considering investing in a prime real estate property in a high-cost area? If so, you’ve likely encountered the term “jumbo loan.” These specialized mortgages are designed for borrowers seeking financing that exceeds the conforming loan limits set by government-sponsored enterprises like Fannie Mae and Freddie Mac. In this comprehensive guide, we’ll dive deep into the world of jumbo loan mortgage rates, exploring their intricacies, challenges, and strategies to help you navigate this unique lending landscape.

What is a Jumbo Loan?

Before we delve into the nitty-gritty of jumbo loan mortgage rates, let’s first define what a jumbo loan is. A jumbo loan, also known as a non-conforming loan, is a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These limits vary by location and are adjusted annually based on housing market conditions.

In most parts of the United States, the conforming loan limit for a single-family home in 2023 is $726,200. However, in certain high-cost areas, like San Francisco or New York City, the limit can be higher, reaching up to $1,089,300 or even higher in some cases.

Any loan amount that exceeds these limits is considered a jumbo loan, and lenders typically have more stringent underwriting criteria and higher interest rates for these types of loans due to the increased risk associated with larger loan amounts.

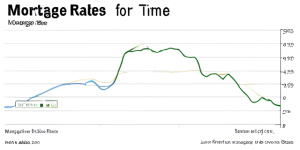

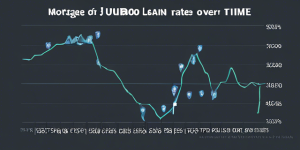

Understanding Jumbo Loan Mortgage Rates

Jumbo loan mortgage rates are typically higher than those for conforming loans because they carry more risk for lenders. Since these loans are not backed by government-sponsored enterprises like Fannie Mae or Freddie Mac, lenders assume greater risk by providing financing without the same level of securitization and guarantees.

Additionally, jumbo loans tend to be more prevalent in high-cost areas, where property values are higher and loan amounts are larger. This increased risk exposure is reflected in the higher interest rates charged by lenders.

It’s important to note that jumbo loan mortgage rates can vary significantly among lenders and are influenced by several factors, including:

Credit Score

Your credit score is a crucial factor that lenders consider when determining your jumbo loan mortgage rate. Generally, borrowers with higher credit scores (typically above 700) will qualify for better rates, while those with lower scores may face higher interest rates or even be denied a jumbo loan.

Down Payment

The larger the down payment you can provide, the lower the risk for the lender, which can translate to a lower jumbo loan mortgage rate. Lenders often require larger down payments for jumbo loans, typically ranging from 20% to 30% or more of the property’s value.

Loan-to-Value (LTV) Ratio

The loan-to-value (LTV) ratio is the percentage of the property’s value that is being financed by the mortgage. A lower LTV ratio (meaning a higher down payment) is generally viewed as less risky by lenders and can result in a lower jumbo loan mortgage rate.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another crucial factor that lenders consider. This ratio reflects the percentage of your monthly gross income that goes toward paying debts, including the proposed mortgage payment. Lenders typically prefer a lower DTI ratio, often below 43%, for jumbo loans.

Property Type

The type of property you’re financing can also impact your jumbo loan mortgage rate. Single-family homes are generally considered less risky than multi-unit properties or investment properties, which may result in higher rates for the latter.

Loan Program

Jumbo loans can be offered through various loan programs, each with its own set of guidelines and requirements. For example, some lenders may offer jumbo loan programs specifically tailored for self-employed borrowers or those with non-traditional income sources, which could impact the interest rate.

Shopping Around for the Best Jumbo Loan Mortgage Rates

Given the complexity and variation in jumbo loan mortgage rates, it’s essential to shop around and compare offers from multiple lenders. Here are some tips to help you find the best rates:

Work with a Mortgage Broker

Mortgage brokers can be invaluable resources when it comes to jumbo loans. They have access to a wide network of lenders and can shop around on your behalf to find the most competitive rates and terms for your unique situation.

Consider Local and Community Banks

While larger national banks may be more well-known, local and community banks can sometimes offer more competitive jumbo loan mortgage rates, especially in their local market areas. These lenders may have a better understanding of the local real estate market and be more willing to work with jumbo loan borrowers.

Explore Portfolio Lenders

Portfolio lenders are financial institutions that hold onto the loans they originate rather than selling them off to investors. These lenders may be more flexible with their underwriting criteria and offer more competitive jumbo loan mortgage rates, as they don’t have to conform to the strict guidelines of secondary market investors.

Negotiate

Don’t be afraid to negotiate with lenders. Jumbo loan borrowers often have more leverage due to the larger loan amounts involved. Be prepared to discuss your financial situation, credit profile, and other factors that may make you a strong candidate for a lower interest rate.

Strategies for Securing Lower Jumbo Loan Mortgage Rates

While jumbo loan mortgage rates are generally higher than conforming loan rates, there are several strategies you can employ to potentially secure a lower rate:

Boost Your Credit Score

Improving your credit score can have a significant impact on the interest rate you’re offered for a jumbo loan. Pay down outstanding debts, correct any errors on your credit report, and maintain a consistent payment history to boost your credit score.

Increase Your Down Payment

A larger down payment not only reduces the lender’s risk but also demonstrates your financial commitment to the property. Aim for a down payment of 20% or more to potentially qualify for lower jumbo loan mortgage rates.

Consider an Adjustable-Rate Mortgage (ARM)

While fixed-rate mortgages are popular for their predictability, adjustable-rate mortgages (ARMs) can offer lower initial interest rates for jumbo loans. However, it’s important to understand the potential risks associated with ARMs, as the interest rate can adjust periodically based on market conditions.

Explore Interest-Only Options

Some lenders may offer interest-only jumbo loans, where you initially only pay the interest portion of the mortgage payment for a set period, typically 5 to 10 years. While this can lower your initial monthly payments, it’s important to understand the long-term implications and have a plan in place for when the principal payments kick in.

Seek Lender Credits

Lenders may offer credits or lender-paid mortgage insurance in exchange for a slightly higher interest rate. While this can reduce your upfront costs, be sure to carefully evaluate the long-term financial implications and determine if it’s a wise decision for your specific situation.

Jumbo Loan Qualification Criteria

In addition to the factors that influence jumbo loan mortgage rates, lenders also consider various qualification criteria when evaluating potential borrowers. Here are some common requirements:

Income and Employment

Lenders will scrutinize your income and employment history to ensure you have the ability to make the larger mortgage payments associated with a jumbo loan. They may require extensive documentation, such as tax returns, W-2 forms, and pay stubs, to verify your income sources.

Assets and Reserves

Jumbo loan borrowers are typically expected to have substantial liquid assets and reserves, often equal to several months’ worth of mortgage payments. This demonstrates your financial stability and ability to weather potential economic downturns or unexpected expenses.

Credit History

While a high credit score is important, lenders will also review your overall credit history, including any past delinquencies, bankruptcies, or foreclosures. A clean credit history with a demonstrated ability to manage debt responsibly is highly valued.

Property Appraisal

Lenders will require a professional appraisal to ensure the property’s value is accurately assessed. This is particularly important for jumbo loans, as the lender’s risk is higher due to the larger loan amount.

Debt-to-Income Ratio

As mentioned earlier, lenders typically prefer a lower debt-to-income (DTI) ratio for jumbo loans, often below 43%. This ratio takes into account your monthly debt obligations, including the proposed mortgage payment, in relation to your gross monthly

Cash Reserves

In addition to having sufficient assets, lenders often require jumbo loan borrowers to have substantial cash reserves, typically equal to several months’ worth of mortgage payments. These reserves serve as a financial cushion to ensure you can continue making mortgage payments in the event of job loss, unexpected expenses, or other financial hardships.

Preparing for the Jumbo Loan Process

Obtaining a jumbo loan can be a more complex process compared to a conventional mortgage. To increase your chances of success and potentially secure a lower jumbo loan mortgage rate, it’s crucial to be well-prepared. Here are some steps you can take:

Review Your Credit

Before applying for a jumbo loan, obtain copies of your credit reports from the three major credit bureaus (Experian, Equifax, and TransUnion) and review them carefully for any errors or discrepancies. Dispute and resolve any inaccuracies to improve your credit score.

Gather Financial Documentation

Lenders will require extensive financial documentation to verify your income, assets, and overall financial stability. Begin gathering the necessary documents, such as tax returns, pay stubs, bank statements, and investment account statements, well in advance.

Consider Working with a Mortgage Broker

As mentioned earlier, working with an experienced mortgage broker can be invaluable when navigating the jumbo loan process. Brokers have access to a wide range of lenders and can help you find the best rates and terms for your specific situation.

Get Pre-Approved

Obtaining a pre-approval letter from a lender can strengthen your position as a serious buyer and demonstrate your ability to secure financing. This can give you an edge in competitive real estate markets and may even help you negotiate a better purchase price.

Shop Around and Compare Rates

Don’t settle for the first jumbo loan offer you receive. Shop around and compare rates and terms from multiple lenders to ensure you’re getting the best deal possible. Be prepared to negotiate and leverage your strong financial position as a jumbo loan borrower.

Alternative Financing Options

While jumbo loans are a popular choice for financing high-value properties, they aren’t the only option available. Depending on your specific circumstances, you may want to explore alternative financing options:

Portfolio Loans

As mentioned earlier, portfolio loans are mortgages that lenders hold in their own portfolios rather than selling them to investors. These loans can offer more flexibility in terms of underwriting criteria and loan amounts, but they may also come with higher interest rates and stricter qualification requirements.

Asset-Based Lending

For borrowers with substantial liquid assets but limited income documentation, asset-based lending may be an option. Lenders in this space evaluate your overall asset portfolio, rather than solely relying on income verification, to determine your ability to repay the loan.

Hard Money Loans

Hard money loans, also known as private money loans, are short-term financing options typically used for real estate investments or renovations. These loans are secured by the property itself and are often provided by private lenders or individuals, rather than traditional financial institutions.

Seller Financing

In some cases, sellers may be willing to provide financing directly to the buyer, either for the entire purchase price or a portion of it. This can be an attractive option for buyers who may not qualify for traditional financing or are seeking more flexible terms.

Conclusion

Navigating the world of jumbo loan mortgage rates can be a complex and challenging endeavor, but with the right knowledge and strategies, securing a favorable rate is attainable. By understanding the factors that influence jumbo loan rates, shopping around, and demonstrating a strong financial profile, you can increase your chances of obtaining a competitive rate and achieving your dream of owning a high-value property.

Remember, patience and diligence are key when seeking a jumbo loan. Work closely with experienced professionals, such as mortgage brokers and real estate agents, to guide you through the process and ensure you make informed decisions that align with your long-term financial goals.

Owning a luxurious or investment property is a significant achievement, and with careful planning and preparation, the right jumbo loan can help make that dream a reality without breaking the bank.

Frequently Asked Questions (FAQs)

- What is the minimum credit score required for a jumbo loan? While there is no universal minimum credit score requirement for jumbo loans, most lenders prefer borrowers to have a credit score of 700 or higher. However, some lenders may consider borrowers with lower scores if they have compensating factors, such as a substantial down payment or significant cash reserves.

- Can I use a jumbo loan to purchase an investment property? Yes, jumbo loans can be used to finance the purchase of investment properties, such as rental homes or multi-unit buildings. However, lenders may have stricter qualification criteria and require larger down payments for investment property purchases.

- Can I refinance an existing jumbo loan? Absolutely. If you already have a jumbo loan and interest rates have decreased or your financial situation has improved, you may be able to refinance your existing loan to secure a lower interest rate or better terms.

- Are there any prepayment penalties associated with jumbo loans? Some lenders may charge a prepayment penalty if you pay off your jumbo loan within a certain period, typically within the first few years of the loan term. However, many lenders have eliminated prepayment penalties, so it’s important to review the terms of your specific loan.

- Can I use a co-signer or co-borrower to qualify for a jumbo loan? In some cases, lenders may allow the use of a co-signer or co-borrower to help meet the qualification criteria for a jumbo loan. This can be particularly helpful if you have limited income or credit history but have a family member or friend with strong financials who is willing to co-sign or co-borrow on the loan.